How Green Book Changes Could Affect Capital Gains

If President Joe Biden’s revenue proposals (the “green book”) for fiscal year 2022 are passed by Congress, fund managers could be facing increased tax liability. One section in the green book identifies carried interest (or profits interest) as a primary source of income to the investment industry. If passed, carried interest — which currently enjoys a preferential tax treatment — would be subject to ordinary tax rates. The proposal also stipulates that individuals with a high net worth or limited partners of funds may also be subject to a new “millionaires” tax.

What is the Current Law?

With the Tax Cuts and Jobs Act of 2017 (TCJA), Congress took its first swing at reducing the benefits that fund managers receive from carried interest on a fund’s performance. Under section 1061 of the Internal Revenue Code, fund managers must now hold a position for more than three years (it was previously more than one year) to receive the preferential long-term capital gain tax rate for gains related to their carried interest. This change primarily targeted hedge fund, private equity and venture capital managers.

Proposed Changes to the Carried Interest Tax Treatment

The current administration plans to further reduce the benefits of carried interest. The green book proposes “closing loopholes” for taxpayers whose taxable income (from all sources) exceeds $400,000. It will effectively treat the carried interest income as if it were ordinary income earned.

The top ordinary individual income tax rate proposed in the green book is 39.6 percent (2.6 percent higher than the current highest rate). If a partner is above the income threshold, a sale of their investment services partnership interest (ISPI) — a carry interest in an investment partnership — would be taxed at the ordinary income tax rate, not the capital gain rate. That said, at least one thing is staying the same: long-term capital gain and qualified dividend income that is allocated based on invested capital — and the percentage of any gain recognized on the sale of an ISPI related to invested capital — would continue to be treated as capital gains.

Additional Taxes Managers Could Face

Per the proposal, carried interest would be subject to self-employment tax (SE tax) instead of the net investment income tax (NIIT). This would add another level of taxes (the SE tax is up to an additional 15.3 percent, with half of the tax taken as an above-the-line deduction). All told, the combined federal income tax plus SE tax could rise to approximately 52.3 percent on the gross of the carried interest income earned. (That doesn’t take into account the SE tax deduction or income thresholds/tax brackets.)

To further add to the tax burden that fund managers face, the green book maintains a $10,000 limit on state and local tax (SALT) deductions. This means that fund managers who live in states with higher income taxes could end up with a tax bill in excess of 60 percent of their gross taxable income. If the proposal is passed in its current form, fund managers in New York and California would be subject to income tax liabilities, based on a gross calculation, of upwards of 65 percent.

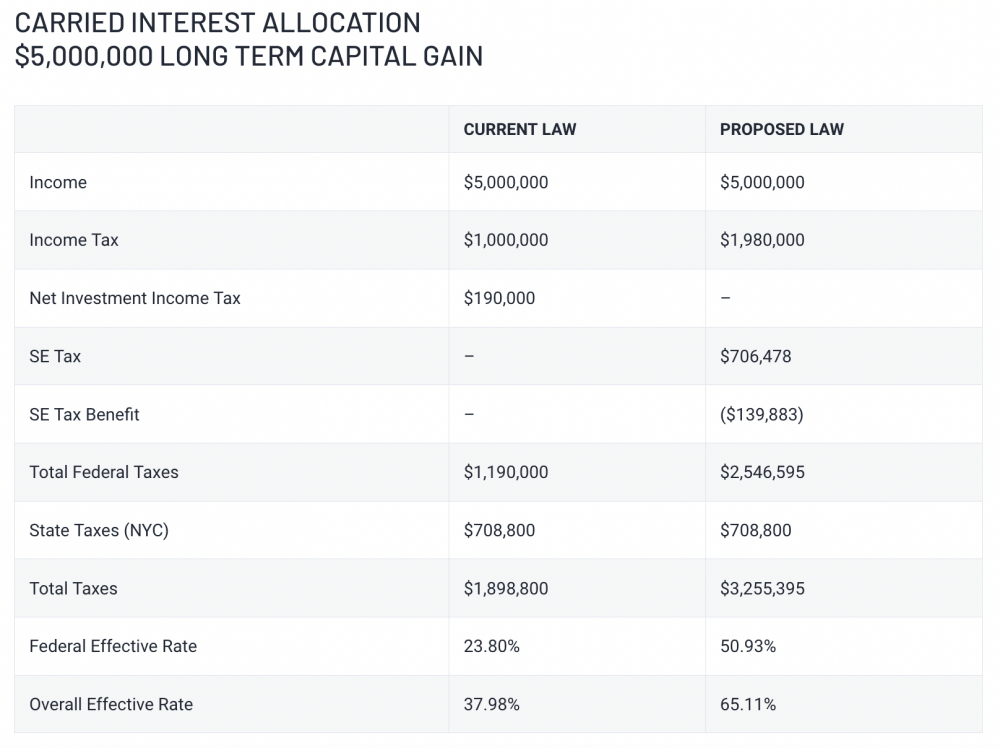

Below is a brief example that illustrates the difference between current tax law and the proposed tax law. The example shows the max individual income tax rates of a fund manager based in New York City who earned a $5,000,000 carry with no other sources of income. Note: The calculation does not take into account the differing tax brackets or SE tax thresholds and adjustments.

The above calculation provides an idea of the additional tax burden fund managers would be subject to if these laws were enacted as proposed. Residents in states with high income tax rates would be subject to an even higher effective rate. The SALT limitation, if removed, could help some taxpayers with the tax burden brought on by this proposal, but the overall tax rate would still exceed 50 percent for many fund managers.

How are Limited Partners or Capital Interest Partners Affected?

In addition to closing the carried interest loophole, the proposal looks to increase income taxes on anyone with an adjusted gross income (AGI) in excess of $1,000,000 in a given year. Although the threshold is higher, the Biden administration did set its sights on capital interest in a fund. A limited partner who obtained their partnership interest via a capital contribution could also be subject to ordinary rates on their long-term capital gains and qualified dividends if the taxpayer’s AGI exceeds $1,000,000 ($500,000 for single filers).

In any year where the taxpayer’s overall AGI exceeds the $1,000,000 threshold, investment income — regardless of tax characteristics — would be subject to the ordinary income tax rate (39.6 percent) plus the net investment income tax of 3.8 percent. This results in a rate of 43.4 percent on the investment income above $1,000,000, meaning that the benefits of holding an investment long term or tying up capital for many years would be greatly reduced. The green book is not clear on how much of the income would be pushed into the higher rates versus the preferential rate, but the book’s general explanations provide the following example:

A taxpayer with $900,000 in labor income and $200,000 in preferential capital income would have $100,000 of capital income taxed at the current preferential tax rate and $100,000 taxed at ordinary income tax rates.

While we don’t know the proposed timing, the new laws would be effective for any gains required to be recognized after “the date of announcement.” Many believe that this date may be April 28, 2021, which is the date the American Families Plan was announced.

Summary

Based on an initial review, the income tax burden on the investment industry is set to increase significantly if these proposals are passed in their current form. Fund documents as they relate to tax distributions may need to be adjusted for the higher income tax burdens that fund managers and their investors will face.

For now, these are just proposals and do not reflect the final documents that will work their way through Congress. As with many prior green book proposals, there is much debate ahead.

This article was originally published on the Marcum Accountants and Advisors website on August 10, 2021.